The available data do not support the hypothesis of price controls or collusive practices in the beef market. On the contrary, they show an intense and systematic transmission of international prices to the price of cattle on the hoof and to domestic beef prices, consistent with the expected behavior in a price-taker country.

Internationally, the Paraguayan beef sector occupies a prominent position due to its degree of global integration. With an annual production of approximately 640,000 tons, Paraguay ranks as a medium-sized producer worldwide (12th place), but its relevance is mainly explained by its strong export orientation. With exports of around 420,000 tons, the country is among the top 10 global beef exporters.

The sector's most distinctive feature is its export orientation coefficient, which reaches 65.9% of total production, placing Paraguay fourth worldwide, behind only New Zealand, Uruguay, and Australia. This indicator reflects a high degree of integration into the international market and, by its very nature, defines the Paraguayan meat sector as a price taker, without significant capacity to influence global prices.

Export Orientation Coefficient Ranking

Source: USDA – Foreign Agricultural Service (FAS), FAOSTAT (FAO – United Nations), SENACSA, and BCP.

This triple ranking—medium-scale producer (12th place), exporter (top 10), and elite export-oriented economy (4th place)—defines the Paraguayan meat sector as highly integrated into the international market and, by its very structure, as a price taker, given that its performance is closely conditioned by global supply and demand conditions, over which it has no significant capacity to influence.

Source: Prepared by the authors based on data from SENACSA, USDA – Foreign Agricultural Service (FAS), FAOSTAT (FAO – United Nations), and BCP.

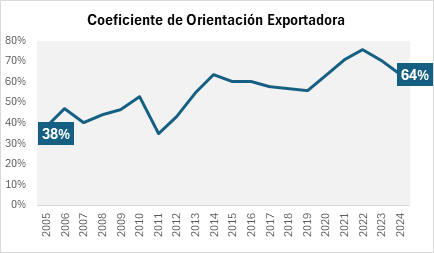

It is important to highlight that the sustained increase in the export orientation coefficient of the Paraguayan meat sector—which rose from approximately 38% in 2005 to around 64% today—is due to a combination of structural and strategic factors. These include the expansion and modernization of the meatpacking plant fleet in a free-market environment.

Additionally, it reflects the progressive adoption of international sanitary standards, the opening and diversification of foreign markets, and a growth rate in exportable supply exceeding domestic market absorption.

From the perspective of its implications, this increase in the export orientation coefficient redefines the economic nature of the sector, reinforcing its role as a price taker in the international market. A larger proportion of production exposed to foreign markets implies a more direct sensitivity to global price cycles, changes in international demand, and market access conditions.

In this context, competitiveness ceases to be a circumstantial advantage and becomes a structural requirement for sustainability, where factors such as production efficiency, logistics, sanitary compliance, regulatory predictability, a free market environment, and diversification of export destinations acquire a central role. Thus, the export orientation coefficient not only describes a statistical fact but also summarizes the degree of integration of the Paraguayan meat sector into the global economy and its strategic dependence on the international environment.